The traditional spring ramp-up in gasoline prices is underway, providing context for understanding why persistent claims of large gasoline price impacts from the Climate Commitment Act are misleading. Gas prices are going up as they always do this time of year, after being surprisingly typical in 2023 and early 2024. After 14 months and 5 regular auctions of Climate Commitment Act implementation, we offer an updated analysis on the Cap-and-Invest program’s impact on gasoline prices, showing that claims often quoted of 50 cents per gallon are inaccurate.

Last September, in an article titled “Do Climate Commitment Act allowance prices get passed through to the pump?” we established a fact-based, dependable baseline expectation for monitoring the price signal of the Climate Commitment Act (CCA) at the pump. In that article, we presented our findings that the most reliable methodology to estimate the gas pump impact of the CCA is a comparison of changing gas prices in Washington relative to Oregon. The growth in this gap reflects the amount fuel suppliers are passing through to consumers and is consistent with partial pass-through. That price comparison was remarkably consistent in 2023 before recently declining to 13 cents per gallon as allowance prices decreased to start year two in a manner consistent with previous Cap-and-Invest systems. In this article, we update our September analysis with another 6 months of real-world data.

EXECUTIVE SUMMARY

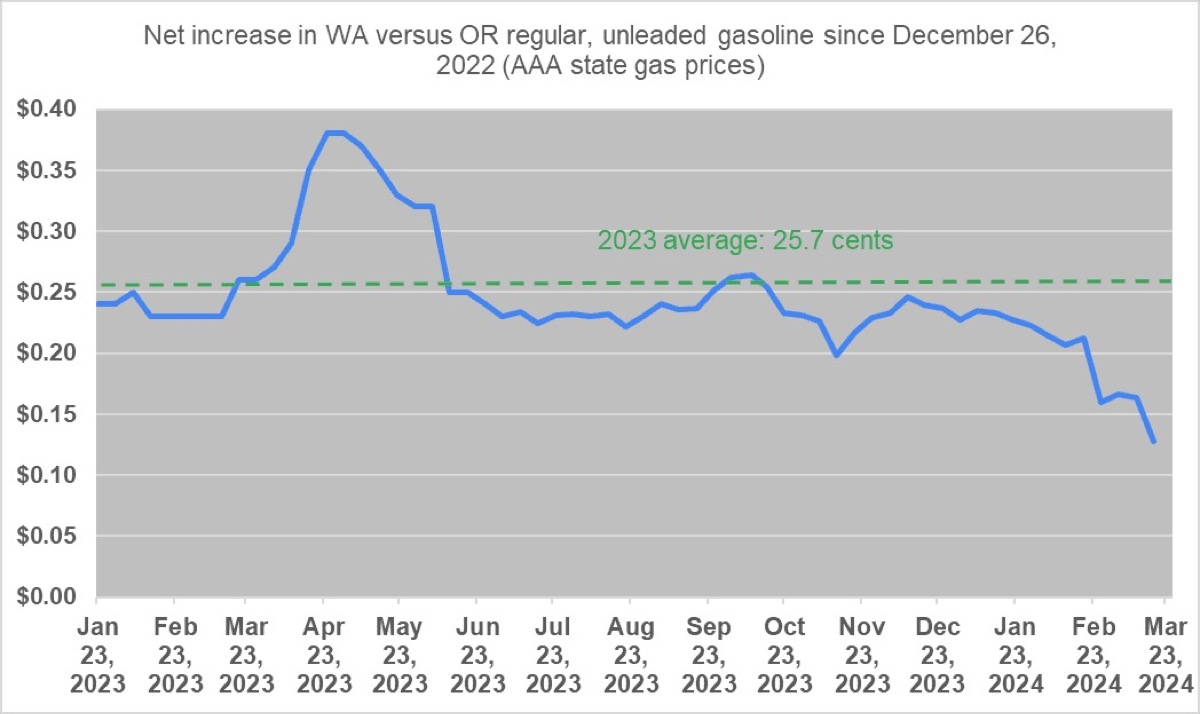

- The best real-world comparison: We have found that the most reliable and accurate measure of the CCA’s impact at the pump is the relative price differential compared to Oregon. Historically, gas prices in WA and OR track closely together, as the two states share supply chains. For 2023, that relative difference was 25.7 cents per gallon more than the historic differential of 11 cents per gallon. To start 2024, it has been even lower: 20.6 cents per gallon through the first eleven weeks of the year, and just 16 cents starting in late February. It was down to 13 cents as of Monday, March 18th, proportional to the decrease in CCA auction prices to start 2024 and reflecting partial pass-through of allowance prices to the pump.

Figure 1: Comparison of increase in Washington versus Oregon gasoline prices relative to late 2022, using a weekly Monday tracking of AAA data between January 23, 2023 and March 18, 2024.

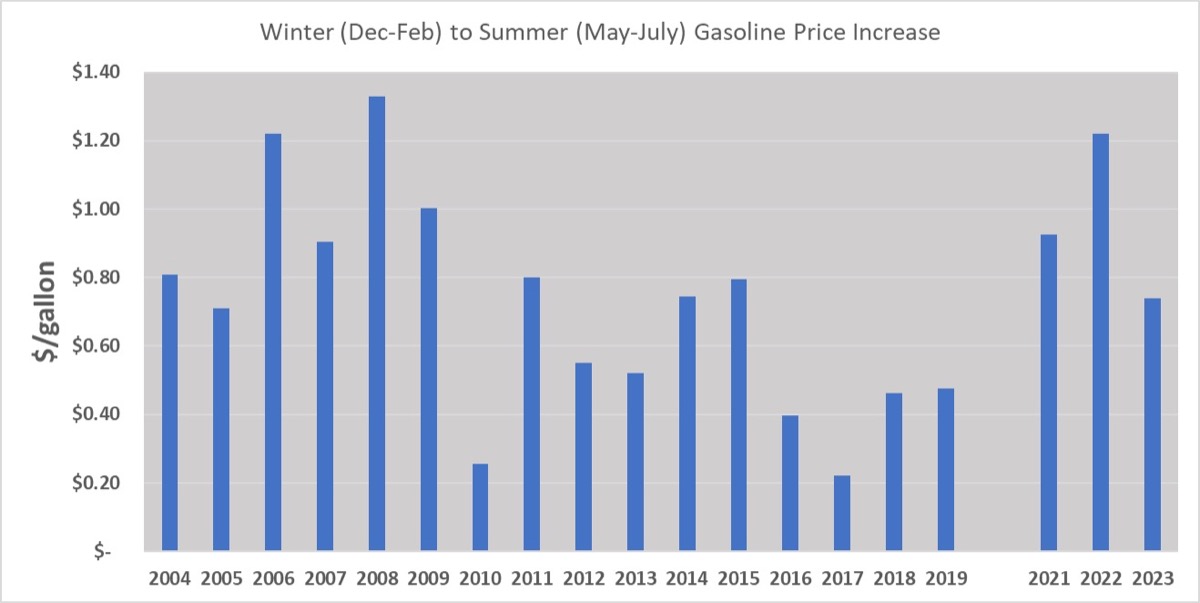

- Surprisingly typical: Real (inflation-adjusted) gasoline prices in 2023 were middle of the pack since 2008, ranking 7th highest out of 16 total years. January and February 2024 prices were both the 9th highest out of 17 since 2008. The annual spring price ramp that we are once again encountering has averaged 74 cents per gallon since 2004.[1] In 2023, the price increase was: 74 cents per gallon. This decades-long pattern is driven by the seasonal increase in demand and refinery switches to summer gasoline blends – and was not primarily driven by the CCA in 2023 as many opponents assert.

- 50 Cents per gallon from the CCA is not accurate: Many claims abound that 50 cents per gallon was (and continues to be) the impact of the CCA at the pump (see some examples in the “50 cents per gallon claims are not accurate’” inset below). However, this relies on a snapshot and an inaccurate assumption:

- Snapshot: Comparisons between Washington and other West Coast States using US Energy Information Agency (EIA) data showed a temporary relative spike in Washington prices of 49.2 cents per gallon in July 2023. However, a full year of data using that metric shows July as an outlier and not a reliable indicator. The full year average (including July) was just 13.4 cents per gallon – yet 50 cents per gallon continues to be frequently cited by opponents of the CCA as documented later in this article.

- Inaccurate assumption: A 50 cent per gallon impact would indicate that allowance prices are more than fully (116%) passed through to the pump. An average of $53 allowance price in 2023, translates to just under 43 cents per gallon based on the carbon intensity of gasoline.[2] Full pass-through is the core assumption embedded in “cap-at-the-rack” calculations and receipts. Recent and evolving research of other carbon pricing programs – documented in our September article – indicates that carbon prices, unlike direct fuel taxes, tend to be less than fully passed through to the end-consumers. Real-world comparisons of WA and OR prices at the pump support these findings.

INTRODUCTION

With gasoline prices beginning their annual springtime rise, we are once again anticipating media interest in Washington state gas prices, and what is driving their increase. From 2004-2023 (ignoring 2020, the only year in which prices declined over the spring due to the COVID pandemic), both the average and median price increase has been 74 cents per gallon (Figure 2).[3] In 2023, the price increase of 74 cents per gallon was exactly in line with historical averages. It’s not a question of if, but how much gasoline prices will increase throughout the spring all across the United States.

Figure 2: The annual, inflation-adjusted, increase in gasoline prices in Washington from winter to summer. Data, including inflation adjustments, are derived from US Energy Information Agency datasets.

It is useful context to consider where Washington gasoline prices have been to start 2024:

- Inflation-adjusted gasoline prices in Washington state were lower in January and February than in any month since April 2021.

- The gap between Washington gasoline prices and USA averages was lower in February ($0.73 per gallon) than at any time in the second half of 2022 – before Washington’s Climate Commitment Act (CCA) was in effect – as well as several months in 2021.

We note that allowance prices at the first auction of 2024 are down from peak 2023 prices, consistent with the year 2 trend we have seen with other cap-and-trade markets. If pump prices were driven by allowance prices (as some CCA opponents claim), then pump prices should also decline. As a leading architect of the Climate Commitment Act, former State Senator Reuven Carlyle, noted following the first auction of 2024: “If prices continue to rise, that will show they move more independently of allowance prices.” We fully expect this to be the case: if matching the long-term average, May-July prices would average $4.77 per gallon after averaging $4.03 in December-February. We do not expect allowance prices to rise by a corresponding amount in the next two auctions.

It is also clear that swings in gasoline prices are much more reflective of trends beyond our state borders. As prices have begun to rise across the country again this spring, Brian Bushard writing in Forbes described the most impactful factors. These factors will continue to dominate volatile gasoline prices until Washingtonians shift away from our reliance on it as a transportation fuel:

Prices hit an all-time high in June 2022, surpassing the dreaded $5 milestone, a major hike made worse by high demand, historically low gas inventories and uncertainty in the international energy market fueled partly by the Russia-Ukraine war.

Turmoil in the Middle East and in Ukraine has also played a role in fluctuating gas prices over the past two years, with recent conflict in the Middle East and the Red Sea threatening to push oil prices further upwards. Oil prices have taken a roller coaster trajectory over the last two years in the wake of Russia’s invasion of Ukraine and as western countries hit Russia with major sanctions. Oil prices skyrocketed last year after Russia and Saudi Arabia, two major oil producers, cut their daily oil outflow, with Saudi Arabia reducing it by 1 million barrels and Russia cutting it by 300,000 barrels (Russia later increased those cuts to 500,000 barrels).

50 cents per gallon claims are not accurate

Claims that the CCA costs residents 50 cents per gallon are still prominent. These claims link most closely back to a temporary price-spike last July (Washington price increase relative to the West Coast which reached 49.2 cents per gallon). However, Washington prices relative to the full West Coast averaged only 13.4 cents per gallon higher in 2023, including this temporary July spike (see Figure 7).

Nevertheless, claims of 50 cents per gallon increase in prices at the pump have persisted – claiming more than full pass-through of allowance prices to consumers! As we showed in our original article, real-world carbon pricing experience suggests less than full pass-through to the pump is typical. Here are some examples of the persistent, but inaccurate, 50 cents per gallon claim:

- Senate Republicans via twitter on March 7th claimed that “the CCA added 50 cents gal/gas, hiked grocery prices, and spiked utility bills.”

- House Republicans still claim the CCA “resulted in a 50-cent-per-gallon increase in gas prices and a 62-cent-per-gallon increase in diesel when it was implemented starting Jan. 1, 2023.”

- In mid-January, Chair of the Washington Republican Party Jim Walsh claimed through a media release that “Contrary to expectations, fuel costs have risen by 50 cents per gallon or more, tripling the expense for consumers compared to the initial information provided to the Legislature.”

- In January announcing his candidacy for governor, Dave Reichert pledged that “On DAY ONE as Governor, I will pause the taxes that are costing you 50 cents more a gallon for gas.”

- In an October interview, founder of Let’s Go Washington Brian Heywood said “Nearly 50 cents a gallon is a huge financial hit for many households…Citizens deserve to have an honest debate on this, not one based on falsehoods.”

- On July 20th, 2023 Western States Petroleum Association released a statement that claimed “Washington’s consumers are now paying 50 cents per gallon for just the cap-and-trade program.”

- Danny Westneat surfaced these claims in June based on an oversimplified and inaccurate calculation, despite no real-world data point at the time indicating a 50 cents per gallon equivalent: “economists and others said the state’s new climate change law is responsible for about 50 cents of that — exactly what the hogwash and baloney prognosticators had been predicting.”

2023 Gasoline Prices: Surprisingly Typical

Given three attempts, can you pick 2023 out from this set of bars which show annual, real (inflation-adjusted) gasoline prices since 2008?

Figure 3: Average annual gasoline prices in Washington state (real, inflation-adjusted dollars) based on US EIA data. Data are randomly, rather than chronologically, ordered.

Now that you’ve made your guesses, here’s some additional context about 2023 gasoline prices:

- Real (inflation-adjusted) gasoline prices in 2023 were middle of the pack since 2008, ranking 7th highest out of 16 total years. January and February 2024 prices were both the 9th highest out of 17 since 2008.

As can be seen from the historical, inflation-adjusted fuel price chart below, gas prices in Washington have long:

- whip-sawed to mirror swings in crude oil prices that are controlled by factors far beyond local control;

- been notably higher than the average US gasoline prices.

Figure 4: Historical, inflation-adjusted, gasoline (left axis) and crude oil (right axis) prices using US EIA data and nominal price adjustments.

Additional Information

Gasoline prices: Carbon price pass-through and real-world data

As we wrote in September and despite claims that all carbon pricing simply reaches the end-consumer, there is strong real-world evidence that carbon prices are only partially passed through. From September’s article:

“A growing body of research suggests that carbon pricing in particular may not fully translate into consumer prices. Assumptions that carbon prices would be fully passed through are often based on experiences with more direct fuel taxes such as excise taxes.”

On this basis, simple assumptions of full pass-through or designations of so-called cap at the rack that are based on full pass-through are an incomplete accounting of the impact on consumers.

Why are Washington and Oregon the most reliable comparison?

The Seattle Times originally noted the consistency in gas prices between the two states, noting that “From 2015 and 2022, a gallon of regular gasoline in Washington was on average 11 cents more than in Oregon.” This consistency makes sense, given the two states, especially the population centers west of the Cascades, are closely linked in supply and distribution with each other but not with other states in the region (see for example this West Coast Transportation Fuels Market report).

What does the Washington and Oregon comparison show after a full year of the CCA?

Washington prices relative to Oregon jumped immediately to start 2023, increasing by a net of $0.24/gallon between December 26, 2022 ($0.11/gallon spread, consistent with the 2015-22 average reported by the Seattle Times) and January 23, 2023 ($0.35/gallon spread). Using AAA state data collected each Monday since then, the relative price increase remained in a tight band of 20-25 cents for most of the year except for a temporary spring peak of 38 cents. Taking the full year of 2023 into account (January 23-December 25) the average weekly increase was 25.7 cents per gallon more in Washington than in Oregon (see chart below). How does that translate to consumers? For a less efficient than average (22 mpg) vehicle with above-average annual usage (15,000 miles per year), this translates to 48 cents per day in added fuel costs.

Figure 5: Comparison of increase in Washington versus Oregon gasoline prices relative to late 2022, using a weekly (Monday) tracking of AAA data between January 23, 2023 and December 23, 2023.

Washington versus Oregon to start 2024:

With the first auction of 2024 complete, we have a benchmark of allowance prices that settled at around half of the 2023 average: $25.76. This has corresponded to a decrease in the gap between Washington and Oregon gasoline prices in recent weeks to a relative increase of 13 cents per gallon as of March 18th. This is down from the 26 cents per gallon gap in 2023, as well as 23 cents per gallon in January and 20 cents per gallon in February. For a less efficient than average (22 mpg) vehicle with above-average annual usage (15,000 miles per year), a 13-cent per gallon increase translates to 24 cents per day in added fuel costs.

Figure 6: Comparison of increase in Washington versus Oregon gasoline prices relative to late 2022, using a weekly (Monday) tracking of AAA data between January 23, 2023 and March 18, 2024.

Less useful (but referenced when convenient) comparisons – the broader West Coast

While it’s helpful to evaluate all the available comparisons, not all are equally reliable. There have been some attempts by others to elevate, particularly when convenient, a comparison of Washington net increases at the pump relative to a wider range of neighboring states. The EIA tracks Washington, California, and regional (West Coast PADD 5, and PADD 5 minus CA) average fuel prices. The comparison of Washington gasoline price increases relative to the full PADD 5 is the likeliest source of 2023 summertime claims that have persisted about CCA raising gasoline prices by 50 cents.

This amount would be greater than full pass-through (average allowance price in 2023 was $53.10, which translates to just under 43 cents per gallon), inconsistent with research that finds the opposite is most likely in carbon pricing programs which are distinct in this regard from direct fuel taxes. We document that research in our September article. A full year of price comparisons versus the same PADD 5 geographies averages to a 9 to 19 cents relative increase in Washington, a fraction of the claimed 50 cents per gallon. Looking at a full year of West Coast data (see chart below), we share three main observations:

Figure 7: Comparison of increased gasoline prices in 2023 versus December 2022 in Washington versus other West Coast states, based on EIA Data.

- There is no consistent correlation between the CCA and the price gap between the regions.

- The gap peaked at the beginning of summer, sandwiched between a long period of low (and even negative) price increases. Focusing on peaks (or valleys), especially when sampled from volatile and weakly correlated comparisons, is a particularly deceptive approach to isolating the program impacts.

- There is no consistent, reliable metric (including the flawed full pass-through of allowance prices) that shows a 50 cent per gallon impact of gasoline prices since the beginning of the Climate Commitment Act.

Conclusion

Bloomberg recently reported on rising global fuel prices, noting that there are, as always, issues far beyond Washington’s Governor or Legislature to control that determine volatile gasoline prices:

Interruptions to fuel production — a combination of scheduled work, unplanned outages and drone attacks on Russian facilities — have been lifting prices. They’ve come on top of higher shipping costs caused by Houthi attacks in the Red Sea and drought at the Panama Canal, as well as the supply-chain ructions spurred by Western sanctions on the Kremlin.

And while more than a million barrels-a-day of new refining capacity is set to come online this year, these projects are notoriously prone to delays. The various moving parts are making it tough to forecast how much fuel will be available in a year where global oil demand is set to break another record and voters in the world’s largest economy will head to the polls.

The Climate Commitment Act has likely had some impact at the pump in its first year, although a much more moderate impact than those opposed to the program have claimed. Unlike previous price swings and volatility, the power of the CCA is that it offers an unprecedented chance to decouple our economy from volatile fuel prices.

While prices have, surprisingly, been quite typical in 2023 and early 2024, we are unlikely to have a strong enough carbon program to insulate us right away from some increased gasoline prices and even bigger price volatility that is beyond local control. However, for the first time in the Evergreen State there is a comprehensive approach to helping Washingtonians move people and goods at a lower cost than we currently do – while delivering positive health, ecosystem, jobs, and climate benefits – and we anticipate that we will see just that if the cap and investments of the CCA are allowed to mature.

[1] May-July relative to Dec-Feb average, in real-terms, which are inflation adjusted to more closely reflect the value of today’s dollar. We exclude 2020’s COVID influenced pricing from this as that is the only year on record with a spring decrease, an anomaly with a clear explanation.

[2] We use the average of all allowances sold in 2023 (41.45 million) which averaged $53.10. If looking only at those generating revenue for the state and excluding those that are consigned (retained by utilities for specified use), the 2023 average was $52.39 per allowance.